Professional Liability Insurance is also referred to as errors and omissions (E&O) insurance. It is commonly referred to as this in the insurance, law and accounting fields. In the medical profession it is called medical malpractice. Professional Liability Insurance is a type of business liability coverage designed to protect traditional professionals who give professional advice and provide technical services for a fee. This coverage is usually in addition to a preexisting General Liability Policy. At the heart of what Professional Liability Insurance does is: ensure consumers have a legal recourse for mistakes made by professionals, and enable professionals to defend and pay damages if they are found responsible.

Accountant’s, Doctor’s and Lawyer’s are not the only professions who have a need for Professional Liability Insurance. There are many types of professionals who are expected to have extensive technical knowledge or training in their particular area of expertise. Some of these others professionals include Insurance Agents, Graphic Designers, Architects, Engineers, Real Estate Agents and Financial Advisers. All of these professionals are expected to perform the services for which they were hired according to the high standards of conduct in their profession. If those professionals fail to live up to the standards of their profession, they can be held responsible in a court of law. This is where Professional Liability Insurance can protect these individuals from litigation that could otherwise ruin their career.

Professional Liability Insurance can also be a benefit when a professional has done nothing wrong. In many instances professionals have claims brought against them or their business for occurrences they are not liable for. Court costs and reputation management costs can be covered in most Professional Liability Policies.

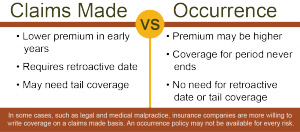

There are certain types of exclusions within Professional Liability Policies. Errors and Omissions Policies typically have specific language and may have strict definitions of what is covered within their contractual language. This makes it imperative for business owners to be honest with their agent about what they are and are not doing within the day-to-day operations of their business.

Professional Liability does not cover bodily injury, property damage, personal injury, or advertising injury claims. Those such claims would be covered under a commercial general liability policy. Most agents should easily be able to design a specific Business Owner’s Policy including all of these coverage’s. This frequently saves the business a lot of cost and ensures there are no gaps in coverage.

So in closing, Professional Liability Insurance is a type of liability coverage designed to protect traditional professionals who give professional advice and provide technical services for a fee. It is designed to ensure consumers have a legal recourse for mistakes made by professionals, and to enable professionals to defend and pay damages if they are found responsible.