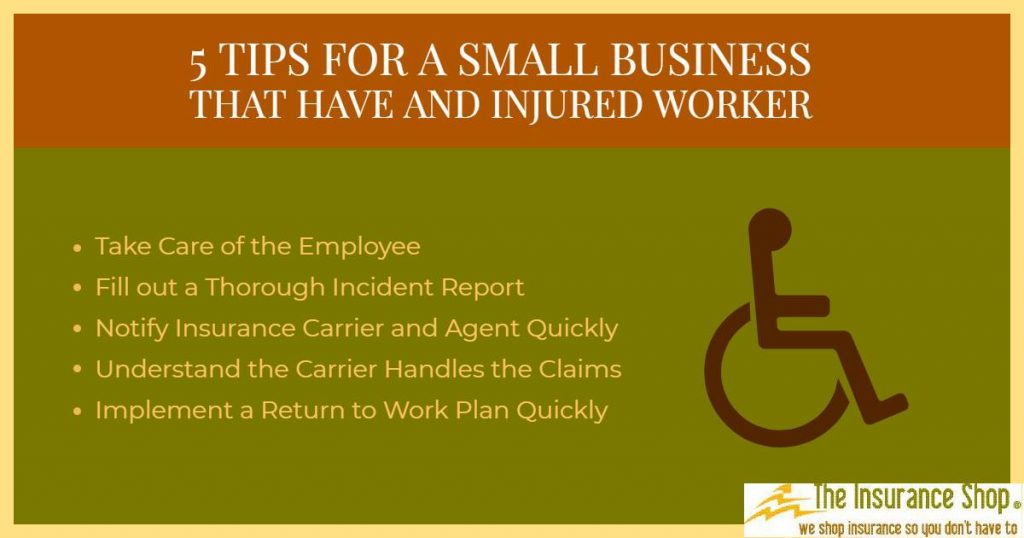

Insurance is one of the biggest expenses for a small business. If there is a way to save, the extra cash flow can help a business immensely. A well-documented safety program are a solid way to lower what a business pays for insurance coverage. An effective safety program does not have to take an enormous amount of time away from your business. If implemented properly the program can cause your business to have less injured workers, lower your insurance premium, lower the amount and severity of claims, prevent your businesses insurance rates from increasing when a claim does occur and it can prevent your business from being dropped from coverage altogether. If a well-documented safety program is implemented properly it will be a win-win situation for both your employees and the bottom-line of your company.

Here are five ways a well-documented safety program can benefit your business.

Less Inured Workers

Safety and preventing injuries is simply the right thing to do. Safety is the right thing for your employees because they will experience less injuries on the job. Safety is the right thing for your business because you will experience less injured workers having to take time away from the job. This will decrease the stress on the rest of your workforce and it will lower or eliminate costly insurance claims that can be a financial disaster for your business. Doing the right thing may seem simple and obvious to most business owners, but many businesses do not take the time to implement a thorough safety program and in the long run it costs them immensely.

Your business can get a better rate on insurance premium

Insurance carriers are more likely to offer your business better credits and discounts if your organization has a well-documented safety program in place. The program shows that your business operates more like a well-oiled machine and less like a rusty old farm tractor. Documentation is especially important to this program. If you do not have documentation of this program, you might as well not have one for insurance purposes. The documentation will help your agent to negotiate better coverage and for the underwriter at your carrier to offer deeper discounts on premium and more credits toward your policy.

Less Severe Claims

When a thorough safety program is in place, the business will experience less accidents. The severity of those accidents will be less. Additionally, if you incorporate a return to work program as a part of the program; injured workers will return to work more quickly. This is extremely important for your insurance policy because the quicker a worker returns to work, even in a limited capacity, the more likely they are to return to work permanently. This can impact the amount of a claim. How much your insurance carrier has to pay out for claims in a given term impacts your businesses experience modification rating. This is one of the few factors that carriers use to determine what they will charge your business for insurance premium. When injured workers do not return to work and stay on workers’ compensation for extended times, it can negatively impact your experience modification rating. This rating along with the industry your business operates in are the two most important factors that determine your rate for insurance premium.

When incidents occur, your business is less likely to have insurance premium rates go up.

When accidents occur; more than likely, your rates for commercial insurance are going to increase. They are less likely to be increased because of just one accident or a string of minor claims, but in the landscaping business eventually a large claim will occur. This is simply the nature of the business. If you have a strong safety program in place, your insurance agent can use the program to explain how the claim is more of an outlier and not a signal of how your organization does business. When a large claim does occur; if a safety program is in place and it is well documented, your insurance agent can use the program to show the underwriter that this incident is not a sign that your business will have more claims in the future.

Safety programs can prevent your business from being dropped altogether.

If you have several claims or one large claim during one insurance term, the insurance carrier may consider refusing to offer coverage moving forward. If this happens and your business cannot find a carrier on the open market to offer coverage for your business you may be forced to buy some coverages from the state provider. For instance, if your business is looking for workers compensation insurance in California you are already operating in the most expensive state in the country to purchase coverage. The assigned risk provider is sometimes referred to as the provider of last resort, the state fund or the state pool. This provider of last resort is typically significantly more expensive than the open market. In most states once you are forced to purchase coverage from the state provider you must continue purchasing from that provider for a period of usually two or three years. This is designed to deter businesses form having excessive claims. A safety program can help prevent this from happening to your business. Just like how your insurance agent can use a well-documented safety program to prevent an increase in premium they can also use it to find some coverage on the open market.